Portfolio Diversification Strategy for High-Income Earners

High-income earners often focus on generating more income, but true wealth creation comes from protecting and diversifying that wealth. A diversified portfolio helps reduce risk, improve returns, and create long-term financial security. By allocating investments across multiple asset classes, investors can withstand market volatility and achieve financial freedom.

📖 Read Complete Guide

Why Portfolio Diversification Matters

Putting all your money into a single asset class exposes you to unnecessary risks. Diversification spreads investments across different sectors and asset classes, reducing the impact of poor performance in any one area.

- ✔ Reduces portfolio risk and volatility.

- ✔ Creates multiple sources of returns.

- ✔ Protects wealth against inflation.

- ✔ Provides better long-term stability.

- ✔ Supports financial freedom goals.

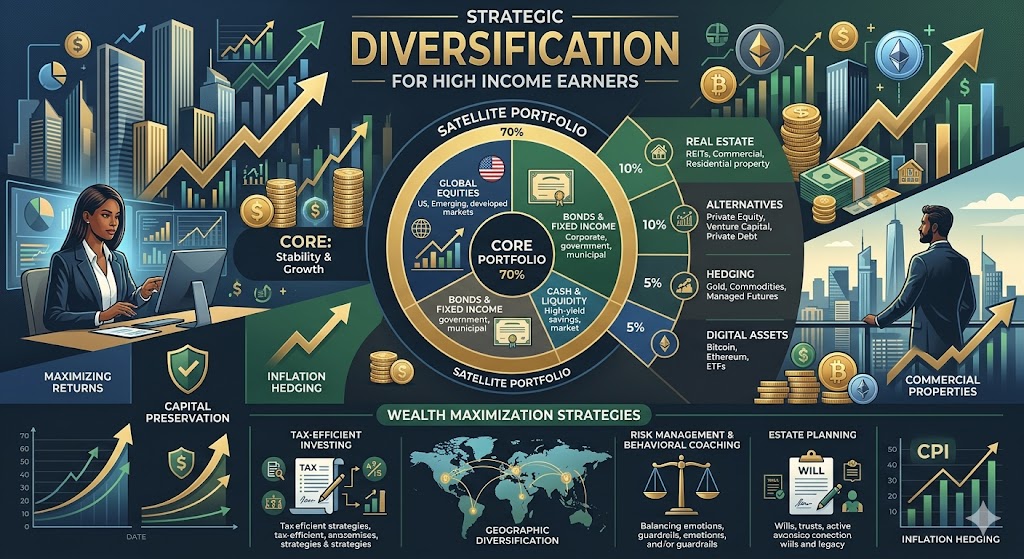

Recommended Asset Allocation

| Asset Class | Allocation | Purpose |

|---|---|---|

| Equity Mutual Funds | 40%-50% | Long-Term Wealth Creation |

| Direct Stocks | 10%-20% | Capital Appreciation |

| Debt Funds & Bonds | 15%-25% | Stability & Regular Income |

| Gold & Precious Metals | 5%-10% | Inflation Protection |

| International Investments | 5%-10% | Global Diversification |

| Emergency Fund | 5%-10% | Liquidity & Safety |

Investment Options to Consider

1. Mutual Funds

Equity, Flexi-Cap, Index Funds, and Debt Funds provide diversified exposure and are suitable for long-term wealth creation.

2. Portfolio Management Services (PMS)

PMS offers customized investment strategies managed by professionals for affluent investors.

3. Alternative Investment Funds (AIF)

AIFs provide access to sophisticated investment opportunities beyond traditional assets.

4. Gold ETFs & Sovereign Gold Bonds

Gold acts as a hedge against inflation and economic uncertainty.

5. International Funds & ETFs

Global investments reduce country-specific risk and provide access to worldwide opportunities.

Risk Management Strategies

- ✔ Review and rebalance your portfolio annually.

- ✔ Maintain adequate Life and Health Insurance coverage.

- ✔ Avoid overexposure to a single sector or stock.

- ✔ Keep an emergency fund covering 6–12 months of expenses.

- ✔ Invest according to your risk profile and financial goals.

- ✔ Maintain long-term discipline and avoid emotional investing.

Who Should Follow This Strategy?

This portfolio diversification strategy is ideal for:

- Business Owners

- Doctors

- Chartered Accountants

- Corporate Executives

- Entrepreneurs

- High-Net-Worth Individuals (HNIs)

- Professionals with High Disposable Income

Key Takeaways

- Diversification is essential for preserving wealth.

- Balance growth, income, and liquidity.

- Regular portfolio review improves performance.

- Combine equity, debt, gold, and international assets.

- Long-term discipline creates financial freedom.

Conclusion

Earning a high income is only the first step toward wealth creation. The real challenge is preserving and growing that wealth efficiently. A diversified portfolio combining equity, debt, gold, international exposure, and adequate insurance can provide stability and sustainable long-term growth. With proper planning and periodic reviews, high-income earners can achieve financial independence and secure their future.

Disclaimer: This content is intended for educational purposes only and should not be considered financial advice. Investment decisions should be based on your individual goals, risk tolerance, and financial circumstances.